Superintelligence for Mortgage Loan Origination

Finally, an AI-native platform that connects originators, borrowers, and operations. Automate work for a faster, lower-cost process. to automate expensive work.

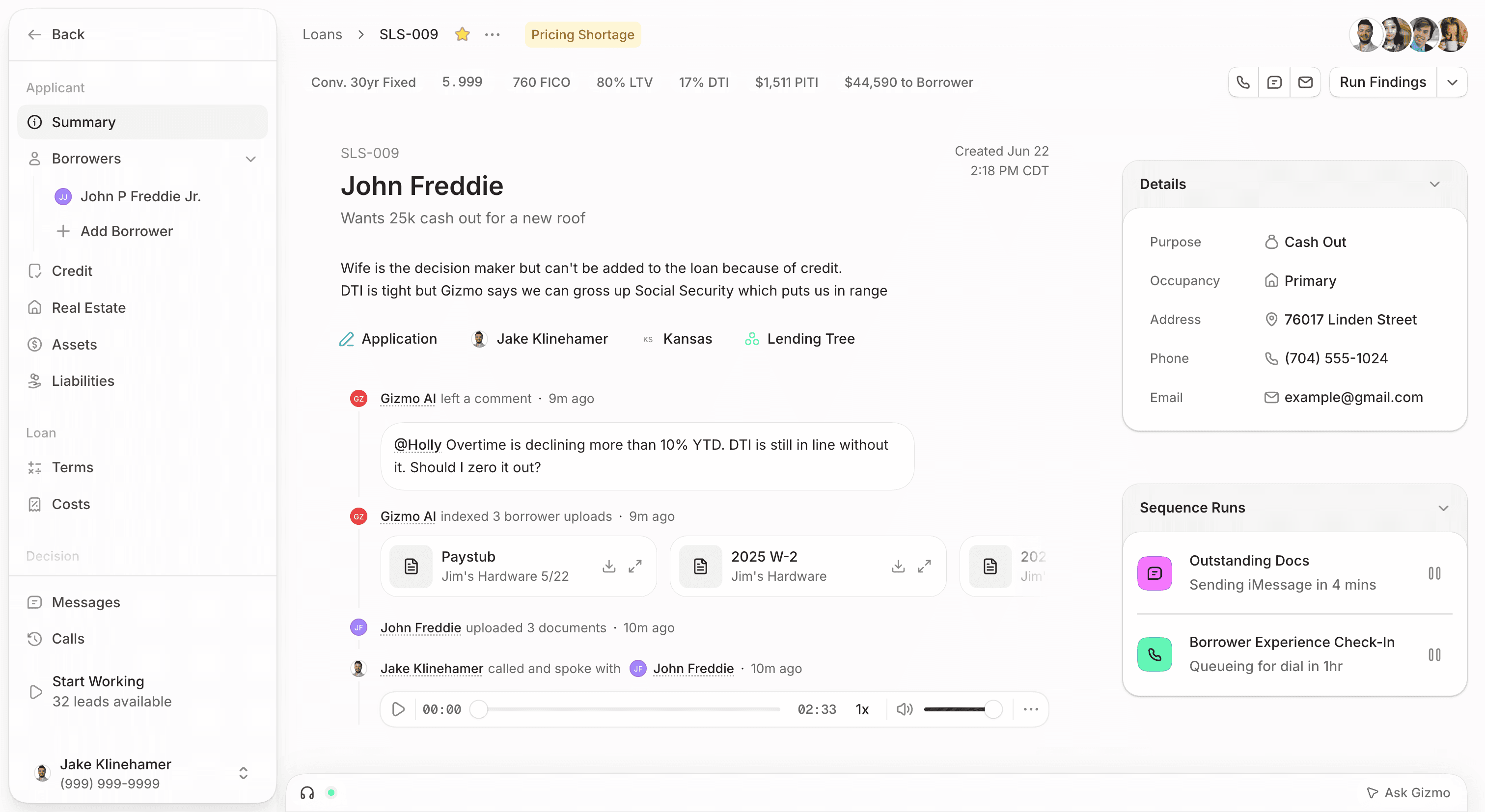

A new class of mortgage tool. Orchestrate work seamlessly across your team and AI agents — without the cost and complexity of managing multiple vendors.

We see a problem here.

At some point in the last 30 years, the industry collectively decided that this diagram was going to be our standard.

Today, lenders are left with the financial and operational burden of stitching together a way for their teams to:

- Manage leads (CRM)

- Accept borrower documents (POS)

- View up-to-date pricing (PPE)

- Communicate with borrowers (Phone System)

Gizmo exists because in 2026, these should be features, not products.

Connect with new borrowers

Turn cold leads into warm conversations that are tracked, routed, and followed up on automatically by humans or AI agents.

Build compliant, profitable loans

Take the guesswork out of loan structuring with real-time pricing, guardrails, fees, and dual AUS to surface what needs attention.

Satisfy closing conditions

Automate loan conditions with AI agents who work alongside your team. Ensure human oversight with human-in-the-loop approvals.

Frequently Asked Questions

Does Gizmo replace our LOS?

Does Gizmo replace our LOS?

Is onboarding complicated?

Is onboarding complicated?

Will our team actually use it?

Will our team actually use it?

Is Gizmo just another CRM or dialer?

Is Gizmo just another CRM or dialer?

What kind of results can we expect?

What kind of results can we expect?